Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor

You can do everything “right” with saving and investing and still fall short of your retirement goals. The real threat isn’t one big mistake, but a series of small, easy-to-miss decisions that quietly drain your future wealth over time. Here’s how those leaks happen and how to stop them before they cost you years of retirement.

If you’re like most people who think ahead, including me, you focus on how much you save for retirement.

Then, you focus on investing for growth (without taking crazy risks).

Get those two items right, and you should be on track for a comfortable retirement after a long career.

That’s what I did.

But there’s a “gotcha” that many people miss. It’s not one big mistake. It’s a series of small ones.

Along the way, you change jobs. Multiple times.

The Bureau of Labor Statistics estimates that, on average, workers change jobs eight times by age 36. Over a working lifetime, it can be many more.

You’ll probably also hit a few “financial road bumps” along the way, or even a “sinkhole” or two.

That’s where the problem often starts.

Because these shocks can cause your retirement savings to leak.

It doesn’t all go away.

In fact, most 401(k) dollars stay in the plan or get rolled over. But for many people, especially those who can least afford it, a meaningful portion slips away when changing jobs or experiencing financial stress.

Quietly. Repeatedly. Almost invisibly.

Over a career, that leak can cost you hundreds of thousands of dollars.

And you may not realize it until it’s far too late.

This article is about the small, normal decisions that can quietly delay your retirement by years and make it less comfortable than it should be.

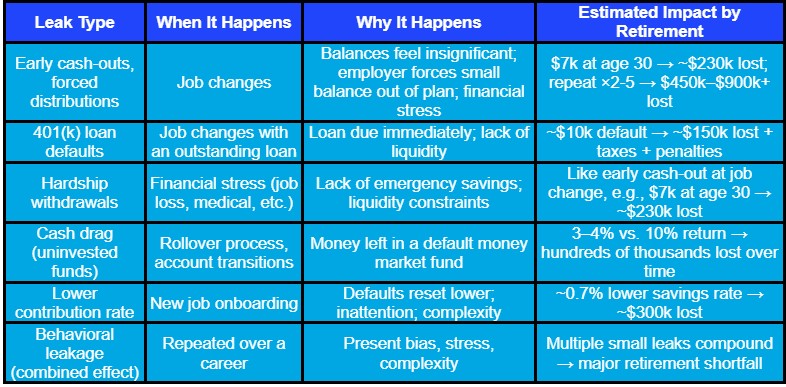

This Could Be the Most Expensive Moment in Your Career (Multiple Times)

You probably don’t think of changing jobs as a retirement decision.

At most, it feels indirectly related through a higher salary or better career opportunities.

But it can be one of the most financially dangerous moments for “future you.”

Because every time you change jobs, you’re forced to decide what to do with your employer-sponsored retirement account.

Leave it (if your old employer allows).

Roll it over.

Or cash it out.

On paper, it sounds simple.

In real life, it rarely is.

You’re leaving a familiar environment and stepping into a new one. One with new responsibilities, new expectations, and often a lot of uncertainty.

This isn’t when you’re at your most focused or deliberate.

And the money you’re deciding about?

It often just doesn’t feel significant. It may feel like a small amount. One you won’t need for years, maybe decades.

And you’re unlikely to get much guidance from your old employer, or your new one.

That’s where the leak can begin.

- You tell yourself it’s not that much money, so it doesn’t really matter.

- You hit a temporary cash crunch and decide to use some of it.

- You have an outstanding 401(k) loan that suddenly comes due, and you can’t repay it.

- You roll the money over but never get around to reinvesting it.

- Your new job quietly resets your savings rate lower (though your shiny new salary lets you save even more).

- Your contributions and employer match end up sitting in a default money market fund.

None of these feels like a major mistake in the moment, or urgent, or permanent.

But over time, they add up.

It looks like “just a few thousand dollars” here and there.

But across multiple job changes and decades, it can quietly turn into tens or even hundreds of thousands of dollars in lost retirement savings.

That translates to delaying your retirement by years or living with a lower retirement income.

Not because you didn’t save.

But because some of what you saved never made it to the finish line, or got stuck in money-market purgatory and never got the chance to grow.

The most expensive retirement mistakes often don’t feel like mistakes when you make them.

You only recognize them as such in retrospect, when it’s too late.

The Impact of Job Changes on Retirement Savings (and Who’s Actually at Highest Risk)

Not everyone leaks money from their retirement accounts.

In fact, most retirement dollars stay invested because people with larger balances tend to keep them invested.

As Vanguard reports, “In 2024, 29% of participants took a cash distribution, but 94% of the assets available for distribution were preserved for retirement.”

But that doesn’t mean it’s only a few people who are affected.

University of Colorado research finds that over 41% of workers cash out at least part of their 401(k) when leaving a job, and 85% of those who do drain the entire balance.

Those aren’t small numbers.

They mean that switching employers quietly sets up far too many workers for massive long-term retirement setbacks.

Sometimes, it’s not even entirely the workers’ choice.

If your balance is small (typically under $5k to $7k), your former employer may force your money out of their plan.

You can roll it over into an IRA. But if you don’t act quickly or don’t know what to do, it may end up in your checking account and get spent instead of invested.

And the impact goes far beyond the amount cashed out.

According to the Employee Benefit Research Institute (EBRI), a non-partisan, non-profit research group, tens of billions of dollars are withdrawn from retirement plans each year through cash-outs alone ($92.4 billion in 2015).

That’s at the high-level system view.

At the individual level, it hits closer to home.

As University of Colorado Leeds Business School Distinguished Professor John Lynch estimates, “Of every dollar that makes its way into a 401(k) plan, 40 cents is withdrawn early.”

These withdrawals trigger:

- Higher income taxes.

- Early withdrawal penalties (if you’re younger than 59½, with some exceptions).

- If you haven’t vested yet, you’ll lose some or all of the employer matching contributions from your account.

- And most importantly, the loss of decades of compounding.

That last one is the real damage.

You don’t lose just the, e.g., $7k you cash out at age 30.

You lose all the growth it cost you.

Invested at a 10% average annual return, those $7k could have grown to over $230k by age 67!

That’s not a rounding error.

It’s years of retirement income lost forever.

What seems like a minor hit, $7k less in your retirement account when you’re 30, robs “67-year-old you” of $10k in annual retirement income!

And that’s just a single job change.

Multiply that by 8, or 12, or 16 times over a working lifetime…

That’s why I say that the biggest retirement decision you make may not feel like one at all.

And most of these choices don’t come from greed or carelessness. They come from trying to survive a rough patch.

And the people who do cash out tend to have three things in common:

- Smaller account balances.

- Shorter job tenure.

- Greater financial stress.

In other words, the people most likely to cash out are the ones who can least afford to.

The Hidden Trap: When a 401(k) Loan Turns into a Withdrawal

Imagine you have a sudden need for cash.

Your options aren’t pretty, especially if your credit score is low and/or you need more money than lenders would lend you.

- Take out a personal loan at interest rates that could go as high as 36%(!) or a credit card cash advance, at rates currently up to 18%.

- Take a loan from your 401(k) plan, with interest rates a point or two above the prime rate, which currently works out to 7.75% to 8.75%.

If offered by your plan, the 401(k) loan is likely the least bad option.

You can borrow more (up to the lower of 50% of your balance or $50,000). No credit check. Interest rates are relatively low, even with a poor credit score. And best of all, the interest you pay goes into your 401(k) balance, so you’re paying yourself rather than a lender.

That looks smart, which is why it’s not surprising that, according to research, 1 in 5 workers have an active 401(k) loan at any given time, and almost 2 in 5 borrow at some point over 5 years.

But there are real risks.

First, if the market goes on a tear while your balance is lower due to borrowing from it, you miss out on a lot of that growth. For example, a $50k loan at 8%, during a year where the S&P 500 returns 23%, costs you over $3k in lost market gains. That’s an “effective interest rate” of more than 12% paid to the market gods.

Sure, the market could tank that year instead, and you’d come out ahead. But that only happens about 1 in 4 years, so not great odds.

Much worse, though, is that while only 10% of 401(k) loans end in default, that’s only if you don’t still owe when you change jobs or get laid off.

If you do, that script flips, because there’s a catch that most people don’t fully appreciate. In this situation, your loan comes due immediately.

And most can’t pay it. Indeed, research shows that fewer than 1 in 7 can and do.

The rest default.

That turns the loan into a de facto withdrawal.

This forced withdrawal is taxable, often with a 10% early withdrawal penalty on top.

And these financial hits happen when you’re likely already under financial stress, so you may be forced to cash out the rest of your 401(k) balance to cover it all.

This further increases your taxes owed.

And the 10% IRS penalty.

One bad hit becomes two.

And what seemed like a smart move initially becomes a trap that quietly turns the loan into a permanent loss of retirement savings.

Not All Leakage Is Spending (The Quietest Leak)

By now, you may be congratulating yourself.

Maybe, like me, you never cashed out a 401(k) balance and never took out a 401(k) loan, let alone defaulted on one.

That does deserve kudos.

But there’s another gotcha…

This one is stealthier, easier to miss. Especially when life gets busy, as it tends to do when you change jobs.

Even if you rolled your old 401(k) balance into an IRA or your new employer’s 401(k). You avoided early cashout, extra taxes, and early withdrawal penalties, but it can still get you.

And you may not notice for years. Or decades.

It comes in two nasty flavors.

The first is lower default savings rates. The second, nastier one, is default asset allocation.

Many 401(k) plans have a default contribution rate of 3%.

That’s good in that it gets new employees, who might not have opted in, to automatically invest for retirement.

But what if you were ahead of that game, having set aside 10% or even 15% of every paycheck into your old 401(k)? If you forget to update your new plan contribution rate, that default would give your contributions an 80% haircut!

If you don’t catch this, estimates show it could cost your retirement nest egg hundreds of thousands of dollars by the time you want to retire.

The second, as I said above, is far worse.

And what if you forgot to tell your rollover IRA and/or new 401(k) how you want your retirement funds invested? Your money could be stuck in default, low-yielding money market funds for months, years, or even decades.

That “cash drag” could cost you huge over time.

Instead of earning an average annual return of 10% or more, your money may be “earning” just 3% to 4%.

And every year this goes on would cost you thousands or tens of thousands of dollars in lost growth that you’ll never get back.

If it continues for years, that could be hundreds of thousands more lost retirement dollars. And while this may not feel like a loss, it is. Because, in investing, what you don’t earn matters just as much as what you lose.

Compounding doesn’t just grow wealth. It also magnifies mistakes, even innocent, understandable ones.

The thing is, nothing dramatic happens overnight. No obvious mistake. No penalties or higher taxes to notice. No notices from your retirement plan administrator.

But the outcome is the same as the other leaks.

Far less money available when you want or need to retire.

Why This Happens (It Isn’t All Bad Decisions)

Even if you make smart choices, you aren’t necessarily safe.

The evidence shows that these retirement leaks aren’t usually due to bad decisions or a giant mistake. They’re most often about people facing difficult tradeoffs, having to make normal decisions at stressful moments.

Decisions that compound in the wrong direction.

Start with financial stress, which is something many Americans face these days.

Retirement leaks don’t typically happen during calm, “under control” situations. They happen when you may be facing:

- Layoffs.

- Medical emergencies.

- Divorce.

- Large expenses (think roof replacement, kids’ college tuition, etc.).

When you’re hit with any of these without sufficient financial resilience, you suffer what economists call “liquidity constraints.”

That’s when you don’t have the cash on hand to handle immediate expenses. Or, in plain English, you need money right now and don’t have enough outside of your retirement accounts.

So, you’re forced to tap those.

You know it’s less than ideal, but it’s the lesser evil.

Next, there’s the timing, which may overwhelm your capacity for making optimal decisions.

If you’ve just lost your job, you’re dealing with a financial emergency, or, on the flip side, you’ve just scored the job of your lifetime. These aren’t moments when you’re in the calm, collected headspace you need for making the best financial decisions.

You’re either desperately trying to stay afloat, or you’re excited beyond words and can’t sit still.

And let’s not forget systemic complexity.

Retirement plans have their own rules, timelines, rollover procedures, and investment options. And let’s not forget the seemingly endless forms.

And all these may change as you change employers, account types, balance sizes, etc.

Even smart, highly educated, financially literate people can get tripped up by all this complexity.

Finally, there’s good old human behavior.

We like to think we’re rational beings with emotions, but in reality, we’re emotional beings who rationalize our emotional decisions afterwards.

We tend to:

- Prioritize the present over the future, a.k.a. poor delayed gratification skills.

- Underestimate long-term consequences, especially when short-term impacts are small.

- Delay what doesn’t feel urgent, a.k.a. procrastination.

Behaviorists call all these effects present bias.

When having a few thousand dollars more in hand today feels more important than a nebulous, long-term loss, that isn’t being irrational. Or at least no more irrational than normal.

It’s called being human.

Pull all these factors together, and you start seeing how human it is to suffer retirement leaks:

- Current financial stress pushes you to take advantage of early access to retirement funds.

- Switching employers creates real financial friction and feelings of urgency.

- Complexity makes it easier to make a poor long-term choice.

And that’s how most leaks get started.

Not all at once.

Not due to stupidity, or carelessness, or lack of discipline.

But quietly, gradually, at predictable points in life.

It’s the result of an imperfect system that requires consistently making perfect decisions, especially when getting them right is hardest.

How to Protect Your Retirement (Without Being Perfect)

This is a lot.

We’ve seen there are multiple ways your retirement savings can leak. And many happen at exactly the wrong time, when it’s hard to do better.

But there is good news.

You don’t need to be perfect to protect your retirement.

You just need to get a few key things right. And you can do some of them ahead of time, when you aren’t stressed out of your mind.

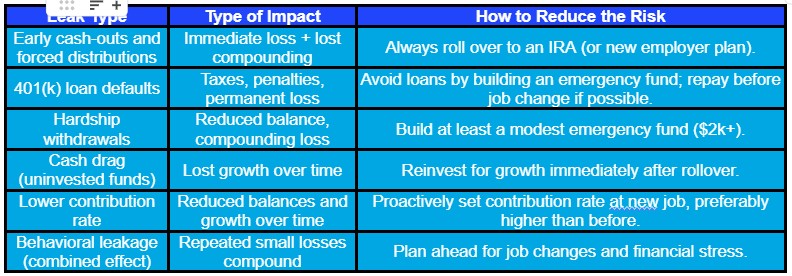

First, build an emergency fund.

Yes, you’ve heard it a million times before.

But that doesn’t make it any less valid.

In fact, Vanguard research concluded that having just $2000 in emergency savings:

- Reduces your risk of needing a 401(k) loan by 19%.

- Reduces your risk of needing a hardship withdrawal by 17%.

- Reduces the likelihood that you’ll cash out your 401(k) by an impressive 43%!

That’s massive!

That $2000 emergency fund won’t eliminate financial stress, but it will give you options, so it’ll be easier to make better long-term decisions in the face of short-term crises.

That’s how even a modest emergency fund can help protect decades of retirement savings.

Next, think of changing jobs as financial moves, in addition to career moves.

Since most leaks happen when people change jobs, it’s crucial to consider those moments through a financial lens too.

When leaving your current job (or any future one):

- Decide what you’ll do with your 401(k) balance (preferably preserving it for eventual retirement, rather than cashing out even small balances).

- If you want to roll it over, initiate that as soon as practical. Once it’s rolled over, deploy it into growth assets as soon as possible.

- When you work with your new employer’s Human Resources people, make sure you sign up for 401(k) contributions that are at least high enough to maximize any matching employer contributions. Then, whether in that 401(k) and/or an IRA, set up contributions at least as high as they were at your old job. If your new salary is higher, increase that savings rate as much as you can. Then, again, allocate those savings into growth assets.

If you take good care of these few things, your future self will thank you heartily.

And remember:

- The more frequently you change jobs, the greater your risk of retirement fund leaks.

- If you’ve made early withdrawals or defaulted on a 401(k) loan before, you’ve already leaked a good chunk of your eventual retirement fund. Don’t compound that damage by doing it again.

- If you don’t have at least a modest emergency fund, you’re increasing the risk for both your present-day self and your future self.

The goal isn’t to be perfect.

Nobody is.

It’s to be aware enough that you set up a few simple habits that make you less susceptible to these risks, especially when life gets messy, as it so often can.

What the Financial Pros Say

As I usually do, I asked some pros to weigh in on all this. Here’s what they had to say.

Q. In your experience, why do people tap retirement accounts early, even when they know it’s not ideal, and what does that tell us about how to plan better?

A. Ben Simerly, CFP®, Financial Advisor and Founder of Lakehouse Family Wealth, says, “People know tapping retirement accounts early isn’t ideal, but the stress of today can be a strong motivator to ignore the potential gains of tomorrow. Tackling the real costs of a pre-retirement cash-out requires a tough look at today’s habits, and most people don’t want to tackle that emotional burden.

“Ironically, the best plan for those tempted to pull funds from their retirement plan early is to simply ignore the account. Sound crazy? Fidelity and other major firms studied this phenomenon and found that, on average, clients who ignore their accounts have more long-term savings than those who log in constantly. There are a lot of exceptions here, but the overall message is important. Being tempted to pull funds or touch money early has real consequences.”

Lucas Fender, Founder & Wealth Advisor at Proper Planning, agrees, “Tapping retirement accounts early isn’t a reckless decision; it’s often a survival decision.

“In my practice, clients who tap retirement accounts early are either bridging a crisis with no other cash available, or they’re changing jobs, and a $10,000 401(k) balance feels like found money rather than stolen retirement. I had a couple come to me in their early 50s who had cashed out three small 401(k) balances in their 20s and 30s, totaling about $22,000. When we ran the numbers, those three ‘small’ cash-outs would have been worth over $190,000 at retirement. That’s the cruel math of compounding. Damage isn’t visible for decades, and then it’s devastating.

“The takeaway for planning is simple… If the 401(k) is the only savings bucket, it will get raided. Every client I work with, we build an emergency fund first. As you stated, Vanguard’s research shows that even as little as $2,000 in accessible savings cuts the likelihood of cashing out a 401(k) early by 43%. That may be the single highest-return ‘investment’ most Americans can make.”

Dr. Steven Crane, Founder of Financial Legacy Builders, shares, “In my experience, people don’t tap retirement accounts early because they’re reckless; they do it because they feel like they have no other option. Job loss, medical bills, helping family, or just poor cash flow planning. It’s usually a pressure decision, not a strategy. What that tells me is that most people don’t have enough margin built into their lives. If your only safety net is your retirement account, it’s not really a retirement account; it’s just delayed spending.”

Q. If you could get people to change just one habit to better protect their retirement savings, what would it be and why?

A. Fender suggests, “One habit I’d change is to treat every job change like a financial event. People land a great new job, accepting the default 3% contribution rate without thinking, while they were saving 12% at their old employer. That’s a 75% pay cut to their future self, and it happens in the time it takes to initial a form. The old 401(k)? It sits in a money market fund earning 3% while the market returns 10%. In investing, doing nothing is still a decision, and it’s usually the most expensive one.”

Crane adds, “If I could get people to change one habit, it would be building a true emergency fund before aggressively investing. It’s not exciting, but it protects everything else. I’ve seen people do everything ‘right’ with investing, but one bad year forces them to pull money out at the worst possible time. That one decision can undo years of progress.”

Q. What about retirement “leakage” do most people ignore, misunderstand, or underestimate?

A. Simerly offers his take, “The most overlooked part of retirement savings is that the money will most likely need to be invested throughout a person’s entire life, not just through retirement age. The benefit of keeping funds invested should be measured by continuing to invest for generations and living off a portion of the gains to avoid running out of money in retirement. When you calculate retirement investment gains through 95 instead of 65, it makes a dramatic difference in the motivation for staying invested.”

“Don’t beat yourself up if this is a topic that’s troubled you and your family; professionals do it too. I doubt there’s been more than a month or two in my career when I didn’t hear an attorney or other professional brush away the differences between the value of money in different account types. At its core, cashing out fails to recognize two core issues. The first is the significant difference between $1 in a savings account and $1 in a 401(k). The two are not the same. The other issue is, why would you ignore your current spending and savings habits? This is a behavioral finance issue, not just understanding the consequences. While it may be an emotional response to ignore the outcomes, knowing the real pain you are inflicting and what you could achieve through some self-reflection could help discourage this behavior.”

Fender says, “People imagine leakage means draining your 401(k) to buy a boat or something similarly reckless. But the real damage comes from a series of perfectly reasonable decisions that compound in the wrong direction over a 30-year career. The biggest blind spot is the 401(k) loan trap. As the statistics you quoted say, one in five workers has an outstanding loan, and most think they’re being responsible. What they don’t account for is what happens if they leave that job before the loan is paid off. The loan comes due immediately, and fewer than one in seven can repay it. I call 401(k) loans ‘an accident waiting for a job change to happen.’ They seem safe until they aren’t.”

Crane wraps things up, “What most people underestimate about retirement leakage is how small decisions compound. It’s not always one big withdrawal. It’s loans that never get repaid, cashing out old 401(k) accounts when changing jobs, or consistently underfunding accounts because current spending keeps creeping up. Over time, those small leaks can quietly derail an otherwise solid plan. At the end of the day, this isn’t just a numbers problem; it’s a behavior problem. The plan only works if the person can stick to it when life gets messy.”

The Bottom Line

By now, you may be wondering how much of your savings actually makes it to retirement.

The news isn’t all bad.

Broadly speaking, especially if you aren’t financially strapped, you can build a large enough portfolio to be able to retire after a decades-long career. That’s why Vanguard data show that about 85% of workers don’t cash out their plans early, and 94% of defined-contribution plan dollars stay in the plan.

But that’s just part of the story.

If your finances are less stable, things become worrisome.

Research shows you’re far more likely to tap your retirement accounts early if:

- You carry debt (and I’m not talking about a mortgage).

- Your balance sheet is weaker.

- You face ongoing financial stress.

In other words, retirement account leakage isn’t random. It follows a pattern.

It’s strongly associated with financial fragility.

And the leak doesn’t usually result from a single big mistake or financial catastrophe.

It’s a repeated pattern of small, completely understandable decisions, usually forced by external constraints.

Job loss pressures your cash flow, forcing you to cash out a small 401(k) balance.

A tough year makes a 401(k) loan the least bad of several bad options.

A change in employers defaults you to a lower savings rate, and possibly to a money market fund that doesn’t offer the long-term growth of other asset classes.

None of these stands out as a horrible mistake. They probably don’t show up as huge financial hits in the moment. In fact, some may show up as a lifeline.

But over time, the long-term impacts compound, pile up, and hamstring your retirement.

Even if you get things “mostly right” and don’t lose everything, enough goes wrong to make your eventual retirement less comfortable and potentially delayed by several years.

Because the biggest risks don’t have to come from bad or even unlucky investments, or poor market performance.

They often result from normal stuff that may seem unrelated.

Repeated career moves, financial stressors, complexity, and human behavior responding to these in a less-than-optimal way.

Your retirement outcome is shaped by how you deal with a handful of predictable moments, including ones that don’t feel important at the time.

Prepare for these moments proactively, and you’ll likely be able to retire sooner with more.

Disclaimer: This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

About the Author

Opher Ganel, Ph.D.

My career has had many unpredictable twists and turns. A MSc in theoretical physics, PhD in experimental high-energy physics, postdoc in particle detector R&D, research position in experimental cosmic-ray physics (including a couple of visits to Antarctica), a brief stint at a small engineering services company supporting NASA, followed by starting my own small consulting practice supporting NASA projects and programs. Along the way, I started other micro businesses and helped my wife start and grow her own Marriage and Family Therapy practice. Now, I use all these experiences to also offer financial strategy services to help independent professionals achieve their personal and business finance goals. Connect with me on my own site: OpherGanel.com and/or follow my Medium publication: medium.com/financial-strategy/.

Learn More About Opher

Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor