Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor

Most people don’t think of themselves as a financial caregiver until suddenly they are one. Whether it’s a parent who can no longer manage investments after losing a spouse, or a sibling whose finances have quietly become unmanageable, stepping into this role is rarely something families plan for. And that’s exactly the problem. What looks from the outside like a straightforward task — helping Mom pay her bills and stay on budget — turns out to involve legal authority you may not have, emotional dynamics no one warned you about, and decisions that require expertise most of us simply don’t have. Financial advisors who regularly work with families in this situation say the gap between what people expect and what they actually face is the single biggest source of costly mistakes. Here’s what they consistently say families miss and what you can do now, before you need to.

“Mom?” I asked, “Have you and Dad set things up so you’d be financially secure if he passed away before you?”

It was 2014.

My concern was that Dad had always handled all their finances. Worse, he was three years older than she was, in poorer health, and, as a male, statistically likely to pass away younger anyway.

Her response was resounding, emotionally driven, and reality-denying: “That won’t happen!“. And that was the end of the conversation.

I didn’t push and never brought it up again. Obviously, neither did she. Like most families, we just left it there.

Two years later, in 2016, what I expected to happen did. Dad passed away, leaving Mom to deal with life on her own for the first time in over 70 years.

In her late 80s, Mom was still perfectly able to handle the day-to-day stuff. She could use credit cards, withdraw cash from the ATM, order groceries, use the phone, and talk with people (though often with less of a filter than appropriate).

Unfortunately, she was woefully unprepared and felt unable to learn how to understand and manage investments, budget appropriately for her situation, or even see how all the moving pieces of her finances fit together. So, I offered to help with managing her finances in Dad’s place.

Given her personality, her experience, and her fears, she didn’t easily trust anyone, not even my sisters or me, to do this. She was afraid that whoever she let in might behave inappropriately with her money, or at least judge her for how she spent it.

So I asked her, “Do you see any situation in this universe in which I would cheat you, steal from you, or even judge you?”

She went silent for a few loaded seconds, then said simply, “No. Never.”

With that acceptance, I stepped in. I thought I knew what to expect. I’d organize things, review her accounts, pensions, and bills; communicate with her investment manager; and make sure she didn’t spend beyond her means. And I did all those things.

Thankfully, Dad had set up the investment management relationship decades earlier, and the CEO there was my oldest childhood friend, so I knew I could trust him. Dad had also set up their credit cards and utility bills to all be paid automatically, so I didn’t have to go too far into the weeds. Not everyone is that prepared and that fortunate.

Mom insisted that she didn’t want to stay in a home that was too big and old for her to manage, where everywhere she turned, there were 60+ years of memories of Dad, and where she’d be alone, with nobody knocking at her door for days at a time.

So, my sisters and I helped her sell her house and move into an independent living facility a few miles down the road, so she knew the area like the back of her hand. This meant that her housing and food expenses were known, predictable, and easily within her means. All that wasn’t the hard part.

One of the harder things was when she couldn’t tell me what various transactions were for, so I couldn’t necessarily separate legitimate expenses from things she’d been talked into inappropriately, let alone outright fraud. Here, too, we were fortunate, and nothing really bad of that sort happened. Much worse, though, was helping her feel comfortable spending her money.

She constantly worried about “Spending my kids’ inheritance.” This, to the point that she wasn’t sure it was ok to buy a few pairs of panties!

This, even though I repeatedly reassured her that she was better than fine, and that I would alert her promptly if I ever saw that she was on an unsustainable path, long before it became too late.

I also had to keep reassuring her that this was her money, that it was there for exactly this reason, that she could spend it as she chose, and that, however much or little remained when she passed away, we’d be happy that she had a comfortable retirement, and grateful for whatever we received.

None of this seemed to stick. She’d say she understood and was ok with it, but as soon as we hung up the phone (I was over 5,000 miles away), she lost the confidence that she could spend whatever she wanted.

In the final analysis, repeatedly giving her “permission” to spend more than she allowed herself, reassuring her that it was appropriate because it was her money and it was there to support her, was more valuable than anything technical I did for her.

Key Takeaways

Financial caregiving is far more than paying bills and monitoring accounts.

Most people stepping into a financial caregiving role expect to handle logistics — paying bills, reviewing statements, coordinating with investment managers. What they don’t anticipate is the emotional weight: helping an aging parent feel comfortable spending their own money, navigating family disagreements, and making high-stakes decisions under pressure with incomplete information and no formal training.

Without legal authority and full financial visibility already in place, families can be locked out when it matters most.

A durable power of attorney, updated beneficiary designations, and a clear record of accounts, income sources, and professional relationships aren’t just paperwork — they’re the infrastructure that determines whether a caregiver can actually act. Families who assume they’ll figure it out when the time comes often discover they’re legally blocked from accessing accounts at exactly the moment their parent needs them most.

The best time to prepare for financial caregiving is long before you need to step in.

Having the uncomfortable conversation while everyone is still healthy — covering where accounts are held, how bills are paid, who the professional contacts are, and what role each family member will play — is worth far more than any planning done during a health crisis. Financial advisors consistently find that the families who navigate caregiving most successfully aren’t the wealthiest ones; they’re the ones who talked about it early and put the right structure in place ahead of time.

The Emotional Side of Financial Caregiving Most People Don’t See Coming

That wasn’t the role I expected to play.

And it’s not a role most people expect when they have to step in to help a parent or sibling manage their finances.

But that, or the reverse, reining in unsustainable spending, may be the most important part of what financial caregiving often entails.

Yes, you have to stay on top of bills, review account statements, pay credit card bills, cancel unused monthly subscriptions, manage investments (or at least oversee investment managers), and handle all the other financial minutiae.

And those, especially if finances aren’t your thing, are hard enough.

But it’s managing the emotional impact of all those daily activities and their implications on the person you’re helping that hits harder.

And in many cases, the problem starts, as it did in our family, years before the people who’ll need the support realize and accept it.

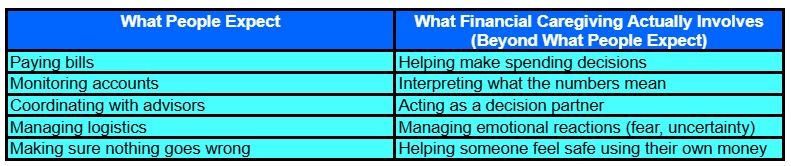

Why Financial Caregiving Is Much Bigger Than Most Families Expect

It’s the gap that catches most financial caregivers off guard.

What they expect when stepping in to help with a parent’s finances is the straightforward stuff:

- Paying bills and credit cards.

- Reviewing account statements.

- Maybe coordinating with an investment manager or professional financial advisor.

But that’s just the start.

As Table 1 shows, the role you’re really stepping into is much broader and deeper.

Yes, you help organize the finances, but you also need to help make decisions on how those finances should (and shouldn’t) be used.

You monitor accounts, but you also interpret what those numbers mean in the context of your parents’ financial life, what they can afford, what they should or shouldn’t do, and how to resolve the trade-offs they face.

It’s not just logistics, as important as those are; it’s the emotional weight they carry, like the fear of running out or of making an unrecoverable mistake.

That’s where things start to get harder.

Because the person you’re helping is already dealing with loss and grief, declining confidence, and a loss of independence and control, when they can no longer manage the things they used to handle on their own or with their spouse.

You’re taking on the unpaid combined role of financial coach, planner, and advisor; investment manager; and tax professional, all with little to no training, experience, or expertise; without a solid framework, and often without a complete picture of the situation you’re helping them navigate.

That’s an extraordinarily heavy and underappreciated load to add on to your already full life, which is one of the biggest things financial advisors point out when working with families in this situation.

The tasks are broader and more complex than most people expect, which is where the most serious mistakes can creep in.

What Financial Advisors Say Most Families Miss

Financial advisors who regularly work with families in this situation consistently point this out.

The biggest challenges aren’t what most people already expect. It isn’t the practical side that you already do for your own family. Getting access to accounts, paying bills on time, monitoring spending, and coordinating with financial pros who’re already in the picture.

You already know how to do all of that, or at least most of it.

And it’s all important.

But you also need to be prepared ahead of time for what’s coming, understand the decisions you’ll be supporting, manage what you should, and recognize where you need professional support rather than trying to do it all on your own.

Dr. Steven Crane, Founder of Financial Legacy Builders, agrees, “The biggest misconception I see is that financial caregiving is just paying bills and managing accounts. It’s not. It’s making decisions under pressure, often without full information, and sometimes with family members who don’t agree.

“The biggest mistakes usually come down to poor communication and no clear plan. Everyone assumes someone else will step in until something goes wrong. Families also tend to wait too long to bring in help. If you’re seeing confusion, repeated mistakes, missed payments, or rising tension, that’s the signal. When emotions go up, and clarity goes down, it’s time to get a professional involved.

“The best thing families can do, long before they’re in that situation, is have the uncomfortable conversation early. Decide who’s responsible, organize where everything is, and outline a plan. It may feel awkward, but that one step can prevent a lot of stress and costly mistakes later.”

But this isn’t just about having help available. It’s also about having the legal authority and access to actually act when the time comes.

That last part is especially important and often overlooked.

As Matthew Fitzgerald, CFP®, Fiduciary Financial Planner at Holistic Planning, Sedona, says, “The biggest misunderstanding I see is that families treat financial caregiving like a task to manage, when it’s really a role that requires legal authority, full visibility, and a plan. The mistake isn’t a lack of love, it’s a lack of access.

“Families often assume they can step in and figure it out when the time comes, but without a durable power of attorney already in place, they can find themselves locked out of accounts at exactly the moment their parent needs them most. By then, it’s often too late to do it the simple way.

“As for when families should stop trying to handle it alone, the signal is usually complexity. When there are multiple accounts, income sources, insurance policies, or healthcare costs that don’t add up clearly, that’s the moment to bring in a professional. But families often wait until there’s a crisis. The right question to ask is: ‘If something happened tonight, would we know where everything is and what to do?’ If the honest answer is no, that’s the moment. And it’s almost always earlier than families expect.

“The one thing families can do today, before they need to step in, is to have a conversation about documents. Not finances, just documents. Where is the durable power of attorney? Has it been updated recently? Who’s named as a successor trustee or beneficiary? That single conversation, done calmly before there’s any urgency, is worth more than any amount of planning done in the middle of a health crisis. The families who navigate caregiving most gracefully aren’t the ones who have the most money. They’re the ones who had the right paperwork and talked about it ahead of time.”

That’s a layer many families don’t even realize exists until they run into it.

In my case, I didn’t fully appreciate until much later how much worse things would have been had my dad not already established the relationship with an investment manager, including automatic transfers into their checking account, and set up auto-pay for all their credit cards and monthly bills, so the core financial infrastructure was already in place.

With all that set up, I didn’t have to manage dozens of financial transactions each month from thousands of miles away, didn’t have to manage a portfolio appropriate for someone decades older than me and on fixed income, consider tax implications, or piece together a full financial plan from scratch.

I could focus on general oversight, interpreting numbers and trajectories for my mom, and helping her feel comfortable spending what she could easily afford.

Many families aren’t so prepared or so fortunate.

When the financial picture is difficult and murky, and when there’s little or no professional support in place, the burden on the non-professional caregiver can become unbearable.

They have to go far beyond their experience and expertise, outside their comfort zone, making critical decisions they’ve never had to make before. Decisions that could have life-changing consequences for someone they love.

Things like managing investments, planning for and managing taxes, crafting a financial plan, and coordinating its pieces.

All for someone in a vastly different financial situation than their own.

That’s the source of the gap between what people expect they’re getting into and what they end up facing.

That’s where having the right support can make all the difference between successfully handling a difficult situation and becoming overwhelmed, burned out, and potentially making costly mistakes.

How to Prepare for Financial Caregiving Before You’re Forced Into It

If I had to do it all over again, I’d do a couple of things differently.

First, I’d have engaged my dad in the first conversations, so my mom’s emotional response wouldn’t have derailed my attempt to help improve her setup.

Second, I wouldn’t simply assume everything would somehow be okay.

I’d have made sure my dad had everything in place that would make things as smooth and clear as possible.

Because if you wait until you’re forced into the situation, your options are more limited.

In my situation, Dad’s knowledge was irretrievably gone. Where they had money and how much, what bills were coming in each month and how they were set up to be paid, how their taxes were being handled, and much more.

When you’re already in the thick of things, you’re reacting during an emotionally difficult time, rather than preparing when things are still calm.

Decisions are harder, more urgent, and more charged.

Learn from my experience: have the difficult conversation while you still can, even if you need to bring it up several times, balancing respect with appropriate, loving insistence.

Make sure you get more than “Everything is taken care of.”

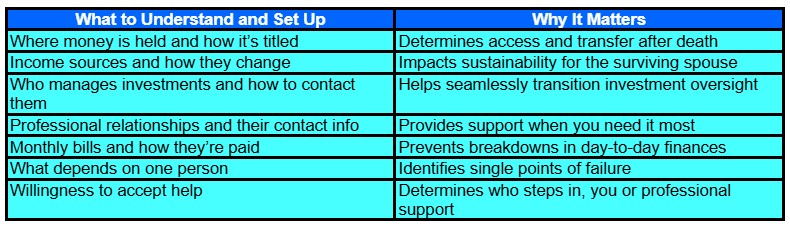

Learn the following (Table 2), and take notes, because you may be fortunate enough to have years before you have to step in:

- What money do they have, where, under what title, and how is it set up to pass to the remaining spouse?

- What income sources do they have, and how will the benefits change once either spouse passes away?

- Who’s managing their investments, what are the account numbers, and how do you reach their point of contact?

- What other professional relationships are in place, and what are the relevant points of contact for those?

- What are the instructions they’ve received?

- What bills are getting paid monthly and how?

- What depends on one person that will break down once they’re gone, unless you step in?

- Will the remaining parent be willing to let you help them? If not, set up professional support for the whole picture.

Pay attention to the hidden complexity.

What decisions require judgment and experience across investing, tax implications, withdrawal strategies, and how everything interacts? And how do your parents want all these to be managed once they need your help?

Be realistic about what role you’re willing and able to play and where you’ll need professional support that isn’t already in place.

Supporting decisions, navigating uncertainty, and helping someone feel comfortable with choices they don’t feel comfortable with aren’t things most of us are trained or prepared for.

That’s where preparation, including identifying the right professionals you can call on when the time comes, can pay off the most. They’ll help you avoid overwhelm and burnout, and handle your new role with clarity and confidence.

Ben Simerly, CFP®, Founder and Financial Advisor, Lakehouse Family Wealth, adds an important shift in how to think about responsibility in this situation, and expands, “The most important part of managing a parent’s finances is giving yourself emotional room to breathe. So many adult children take on managing their parents’ finances with zero guidance, zero help, and zero preparation from the parents. In this kind of scenario, give yourself permission to be human, take some deep breaths, and let the guilt go for decisions you had no part in that put you into this position.

“As an adult child, it’s your responsibility to help care for your parents. But it’s your parents who are responsible for setting up a plan, putting the right professionals in place, and providing assistance far beyond a will, power of attorney, and medical directives.

“The biggest mistakes we see are when aging parents don’t create any detailed plans, numbers to call, processes, or directives beyond the core legal documents. In short, while the legal documents provide theoretical authority, they rarely provide direction. Every estate plan needs direction in addition to the core legal documents.

“More often than not, if they aren’t in place already, a financial advisor, a tax accountant, and an estate planning attorney should be calls number one, two, and three after finding out you need to step in to help manage finances. In some scenarios, they may not be required beyond an initial phone call or two; in others, they will. But even for experienced pros, it can be difficult to decode how someone set up their financial life. What you don’t know can hurt you and your loved ones.

“The better estate attorneys and financial advisors consider planning beyond the core legal documents with instructions, final wishes, and real instructions as an absolute bare minimum foundation in estate planning. And remember, estate planning ties directly into advanced care and health care planning while aging parents are still living. In short, make sure every estate plan includes the required legal documentation, but also plain-language instructions for what to do when something happens. Your entire family will thank you.”

Taken together, this is what financial caregiving really demands: more preparation, more support, and more clarity than most families expect.

The Bottom Line on Financial Caregiving: Why Preparation Is Everything

Financial planning isn’t something most of us expect, let alone plan for.

We fall into it, mostly when we’re already emotionally reeling from loss and grief.

And when we do, we discover it’s not just about managing money the same way we already do for our family. We suddenly need to manage someone else’s decisions, uncertainty, and emotions. Someone we love, who’s struggling with grief, loss of independence, and potentially diminished capacity.

This is all a lot.

And most people underestimate it until it’s too late and they hit and exceed their limits.

I was fortunate in ways I didn’t fully appreciate at the time, but it was still a big challenge, despite not having to do it all on my own.

Most families don’t have that level of preparation and support already built in.

That’s why the most important thing you can do now isn’t just to be willing to step in when the time comes. It’s to fully appreciate the breadth and depth of what you’ll be signing up for, ensure you have all the information you’ll need, and know who you’ll call on when you need support.

Because if you’re forced to enter the support role without all that prep work done, you’ll likely be overwhelmed and unable to do the kind of job you’d want to do for your parents.

Disclaimer: This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

About the Author

Opher Ganel, Ph.D.

My career has had many unpredictable twists and turns. A MSc in theoretical physics, PhD in experimental high-energy physics, postdoc in particle detector R&D, research position in experimental cosmic-ray physics (including a couple of visits to Antarctica), a brief stint at a small engineering services company supporting NASA, followed by starting my own small consulting practice supporting NASA projects and programs. Along the way, I started other micro businesses and helped my wife start and grow her own Marriage and Family Therapy practice. Now, I use all these experiences to also offer financial strategy services to help independent professionals achieve their personal and business finance goals. Connect with me on my own site: OpherGanel.com and/or follow my Medium publication: medium.com/financial-strategy/.

Learn More About Opher

Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor